CLOSING THOUGHTS

There you go, one weird day as the NAZ closes slightly lower with positive internals, the SPX closes down 3 with flat internals and the DJIA closes down 32 with 6 higher and 24 lower. And of course the IWM closes up about .5% to make put the icing on the cake.

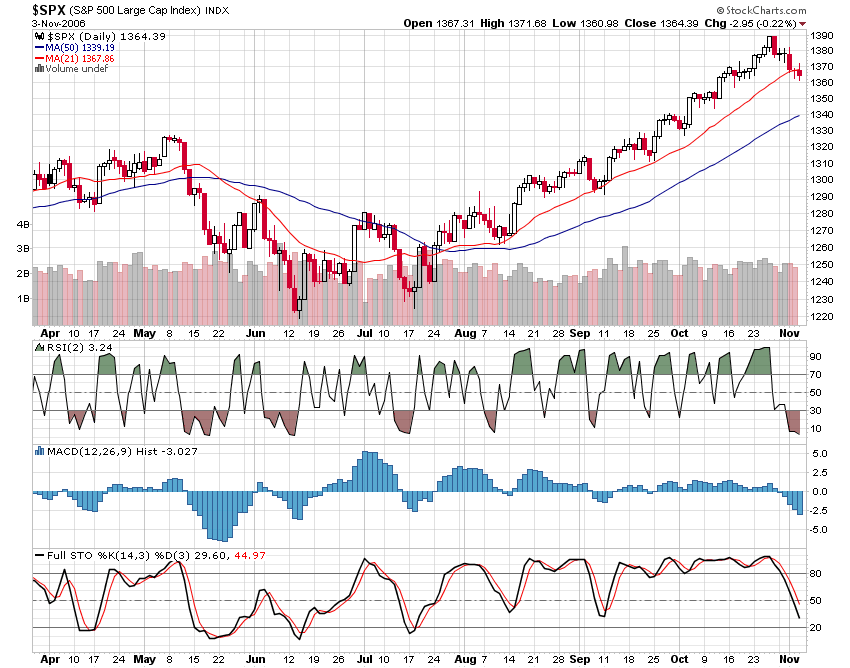

There you go, one weird day as the NAZ closes slightly lower with positive internals, the SPX closes down 3 with flat internals and the DJIA closes down 32 with 6 higher and 24 lower. And of course the IWM closes up about .5% to make put the icing on the cake.Anyhow, the SPX closes with a 2 day RSI of 3 and is back at the 1,365 inflection point. The DJIA is acting a bit worse and is a bit below the 12,000 mark. Keep your hat handy as it may cross again next week when the "journalists" at CNBC cheer lead the big caps higher.

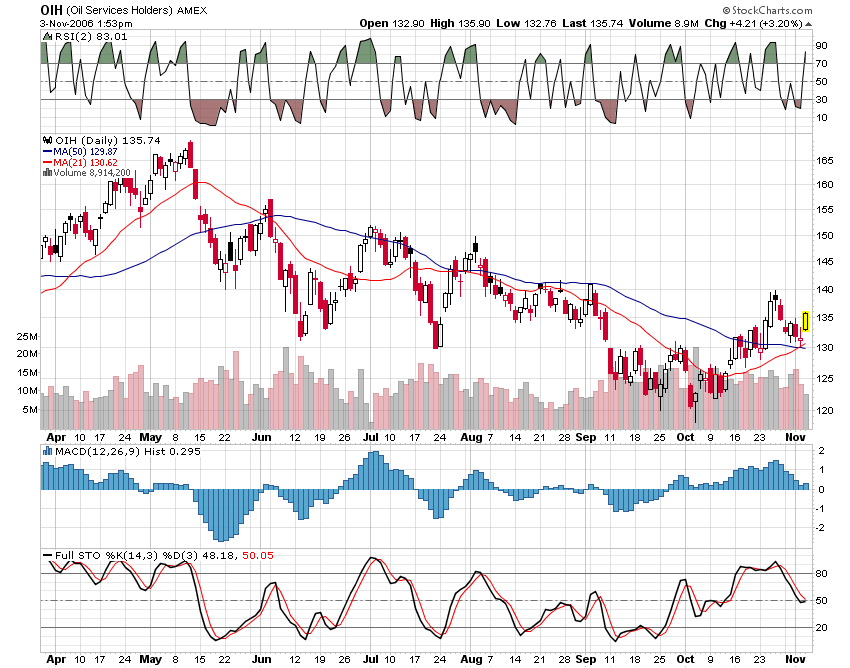

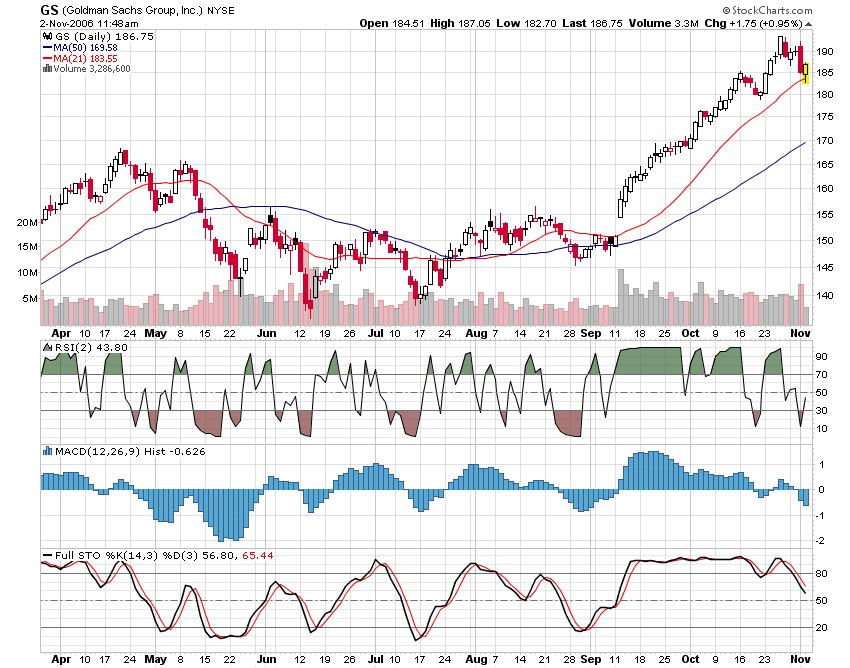

Sector winners today included oils, metals, small caps and biotechs. Biggest losers, retail, brokers and trannies.

posted by DAVID at

4:10 PM

0 Comments

![]()