Listening to the genius of CNBC and at CNBC generally makes me want to pull my hair out ( and I have plenty) as they continue to get much of what they say exactly wrong. This afternoon Dylan et al were blabbing about the action in the financials and how they were leading the markets higher in light of the great earnings reports from the brokers.

Well, the sector leaders were RETAIL, SEMIS, TRANNIES, OILS, HOMIES and TECH. Brokers (XBD) were up .6% and the Banks (BKX) were up .64%. The IAI, which is an ETF of brokers with the biggest such as GS MER and MS getting the greatest weight, was up 12 cents or .22%. Thanks for the great information. I never thought I would anxiously await a product from FOX but I am curious as to what they will offer with their new financial network. If I could trade it I would short CNBC in size and go long FOX despite the fact that they are a wholly owned subsidiary of a political party.

Anyhow, the worst performing sectors were airlines, GOLD, SILVER, reits, utilities and biotechs.

Market internals closed with 900 more winners than losers on the NYSE and 530 more winners than losers on the NAZ. These numbers are way off the highs of +3,000 which occurred early this morning near the open and I suspect this does not bode well for tomorrow and we will see what we see for next week.

Also, check the NAZ Futures, they hit a high of 1,834 at 10:40 and closed the day at 1,824, also considerably off the highs as was the IWM which peaked earlier in the morning and closed up .5% back at $79.02.

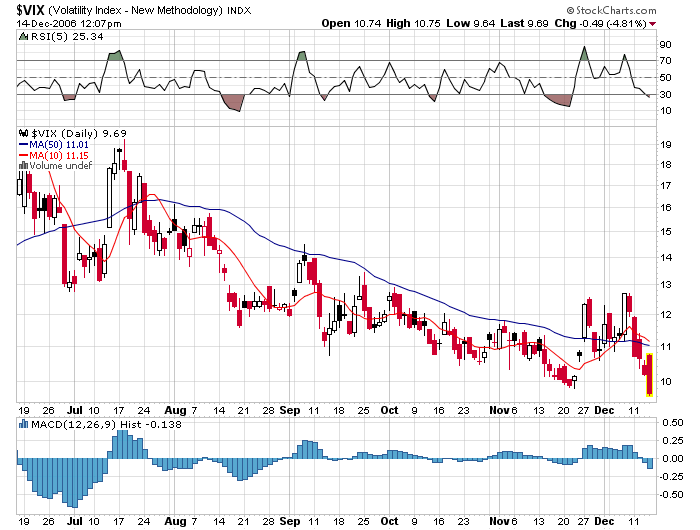

The VIX/VXO tandem is giving out sell signals as both close under 10 and in excess of 10% below their respective 10 day SMA's. The 2 day RSI on the SPX/DJIA gives another sell signal with a reading of 96 and the QQQQ downtrend remains intact as the high from November 22 is still a bit away.