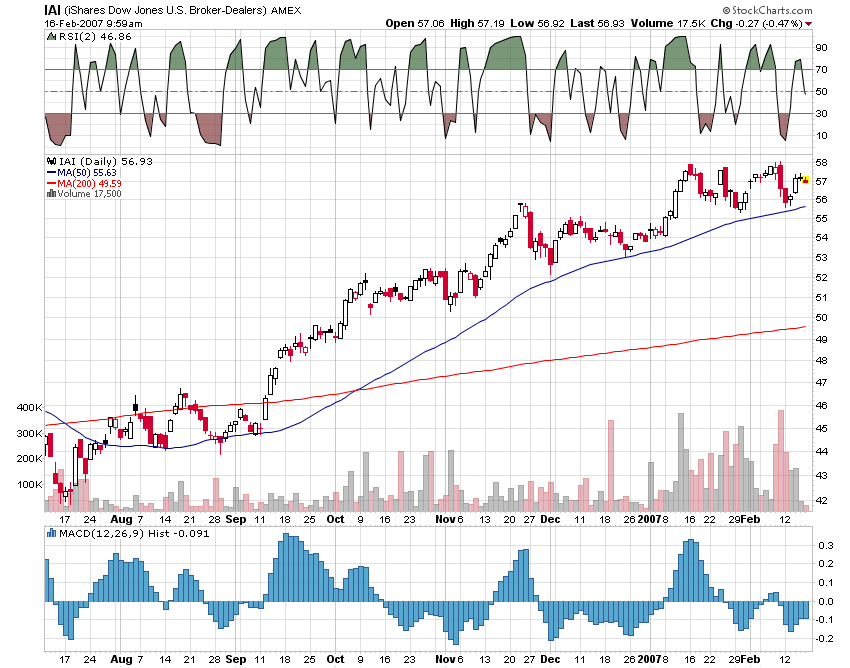

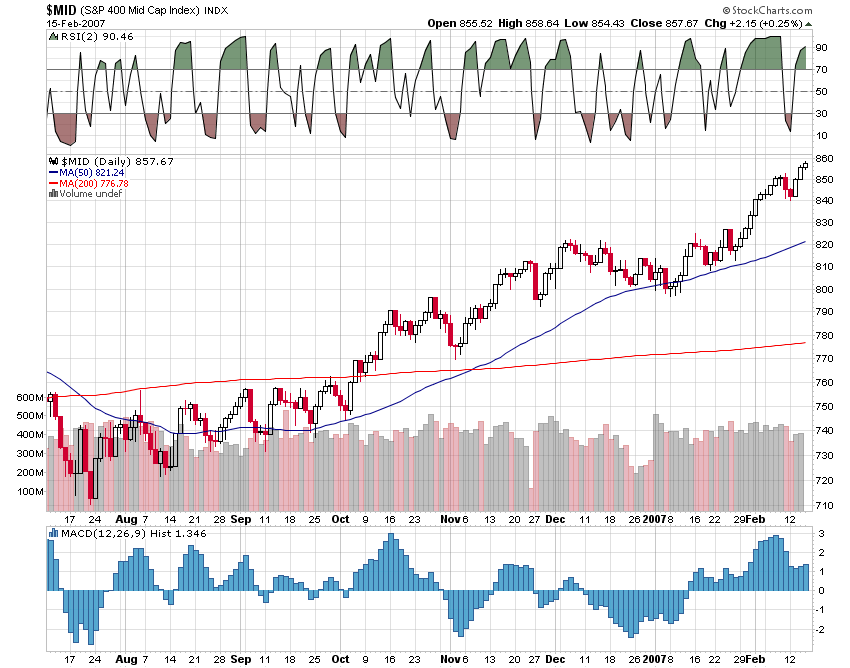

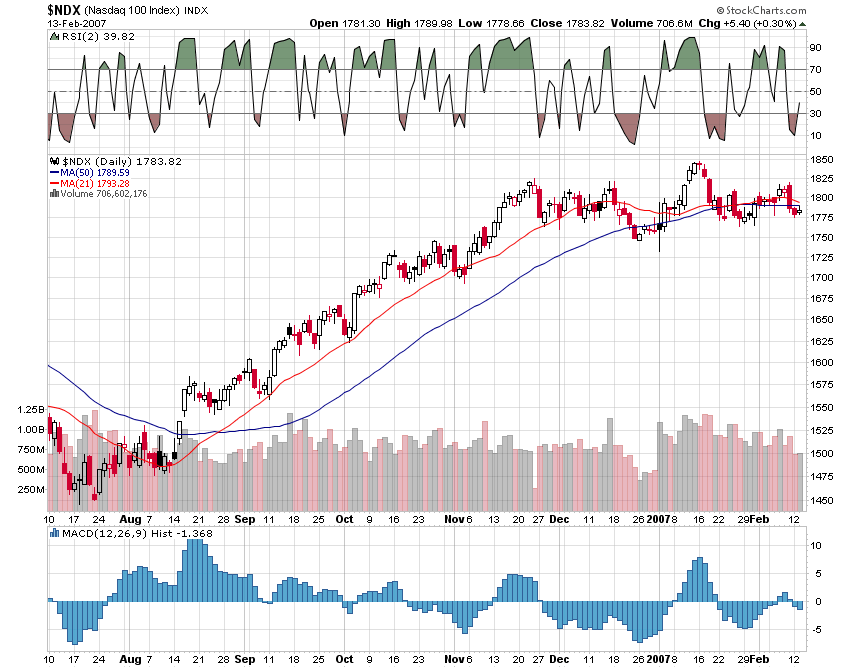

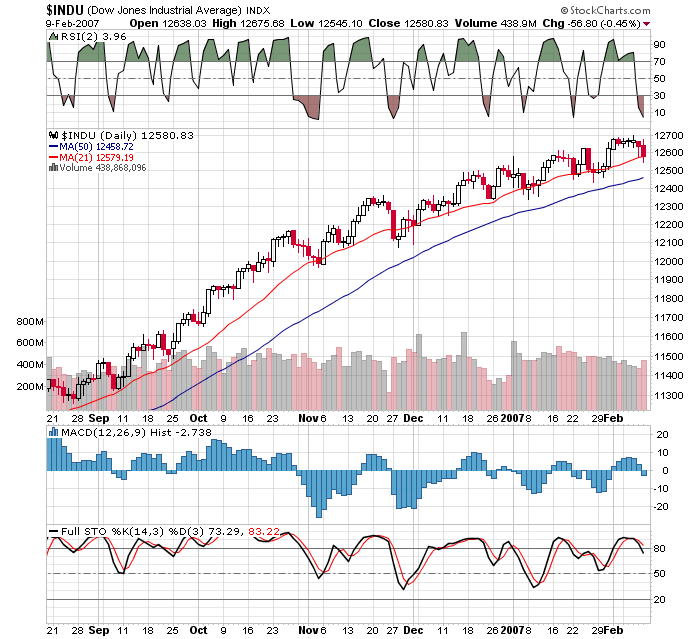

Checking the technicals on the DJIA, the markets are short term oversold with the 2 day RSI under 5 and the index trading at its 21 day SMA. Needless to say, those spots have been pretty good buying areas in the past. Is it different this time? Could be, but the trend lines point higher and buying dips has been the winning trade for several years.

On the news front:

WSJ reporting that TRB to forego bids and go it alone; Saudi oil minister says market is balanced; UBS upgrades KFT to to Neutral from reduce; CIBC upgrades Q to sector perform; AG Edwards upgrades JWN to Buy from Hold; PRU defends MA and reiterates $130 target; AAPL upgraded to Buy from Hold at C with a $105 target; HOC beats by 1 cent, revenue rose by 15.5% to $938M v $793.2M consensus and raises the dividend 25%; London Times reporting the

BMY SNY merger seems to be off; FS confirms it will be taken private at $82 per share cash;

Barron's positive on UNH and COST while Art Smith from John Herald was very bullish on certain oil companies like CHK CNQ APC APA ECA LINE and EVEP.

Here is some of what he said:

"According to our president, we are addicted to oil, but apparently we don't want to explore for it anymore.

All of the data we collect show the industry's capital investment in the upstream -- for exploration, anyway -- has been declining substantially from where it was five and 10 years ago.

It amounts to 15 cents on the dollar when it used to be 30 cents on the dollar.

Basically, the

exploration model hasn't been working, so no one is funding it. The big oil companies have determined the best thing they can do is continue to buy in their own stock and pay dividends.Our bottom line on this exploration paradox is that

it will cause the large companies to review all the major players in the world, and those that have undeveloped reserves of significant magnitude but require capital will be the targets. Major oil companies have become bankers, rather than risk-takers.I am amazed at how the market is influenced by very modest changes in estimates of natural gas inventories or estimated demand. We are talking about 85 million barrels a day of oil being consumed and the market will sell off on a change in estimates of 100,000 barrels a day or in gas inventories of 10 billion cubic feet, which is a rounding error. All the evidence suggests the market is tightening and reserve additions are disappointing, and we are back in the King Hubbert and peak-oil discussion.

The most undervalued on the basis of a reasonable price tag are the North American exploration and production companies. There are probably 50 companies, but among the ones that are most undervalued are Anadarko Petroleum [APC] and Chesapeake Energy [CHK] and Apache [APA].

We like some of the Canadian companies, EnCana and Canadian Natural Resources, which have tremendous resources in countries that are safe and where you can make a profit. In the case of Canadian Natural [CNQ], for instance, they have an enormous oil-sands investment whose substantial production and profit value is just becoming visible."